CONTRIBUTORS

NEIL GIBSON

CEO, UK, Sedgwick

GAIL OLIVER

SVP, Sales – Property Americas, Sedgwick

MANDEEP SANDHU

VP, Environmental Service Line, EFI Global

PETER WASSELL

Technical Director, UK Repair Solutions, Sedgwick

Slowly but surely, the world is coming to recognize that Earth’s climate is changing; it’s hard not to. Over the past decade, we’ve seen extreme temperature swings and devastating weather-related catastrophes, from floods to droughts to hurricanes and more. As a result, addressing the realities of climate change with innovative solutions that promote resilience among all stakeholders has become a strategic necessity for everyone — from the CEO of a major European corporation to a homeowner in Florida.

Climate change has far-reaching implications, including a profound impact on the businesses, people and communities that rely on insurance carriers, third party claims administrators (TPAs) and supporting industries to protect their homes and livelihoods.

To survive, all will need to adapt and evolve. In our industry, a common model for tackling change is to break it down into three key steps.

- Ready

- Resolve

- Recover

Here, we will further explore each of those actions and outline ways we can work together to address the ongoing challenges of our changing climate.

Readiness to make the necessary changes

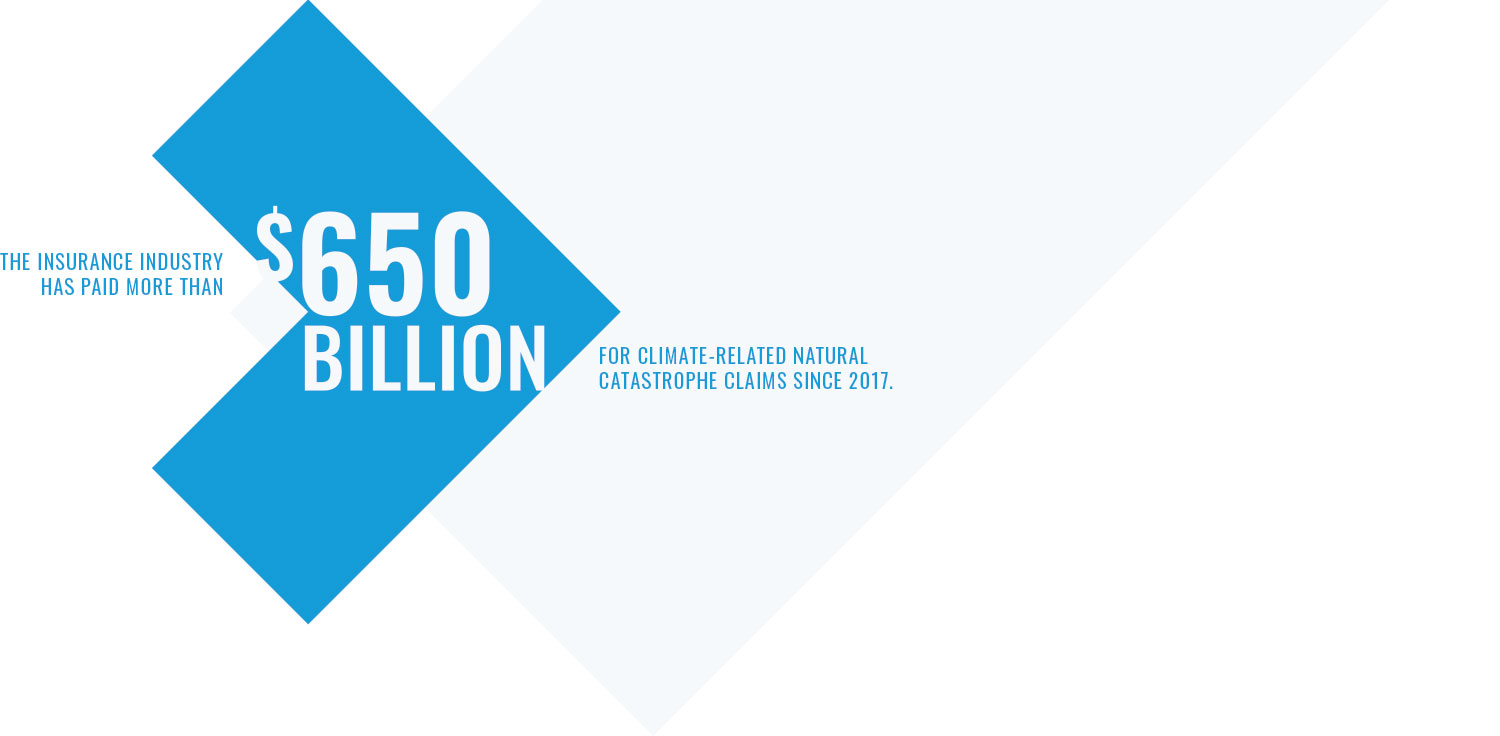

One of the most direct impacts of climate disruption is the increase in claims due to more frequent and severe weather-related events. Insurance Journal reports that the insurance industry has paid more than $650 billion for climate-related natural catastrophe claims since 2017.

While this data is troubling, the good news is that some organizations and governments are now taking bold steps toward combating climate change. These encompass everything from reducing greenhouse gas emissions (GHG) to supporting and educating businesses and consumers on preparedness for ongoing climate-related events.

Another critical area for any entity or individual preparing for weather-related claims is routinely checking their insurance policies for adequate coverage. Due to inflation, a building operating under a policy bought 10 years ago could be grossly under-insured today. Close examination of policies with brokers and other trusted professionals is crucial to catastrophe readiness.

While some insurance carriers are increasing premiums or choosing to exit markets that are high-risk for catastrophic events, many have developed new policies to address climate change. As highlighted on the Sedgwick blog, there are a number of steps businesses can take to address their shifting coverage options, including:

- Thinking beyond traditional insurance — transferring risk, exploring self-insurance, and looking at options like parametric insurance or catastrophe (CAT) bonds

- Building a risk map to identify areas of need and monitoring weaknesses by forecasting climate change impacts

- Focusing less on the annual insurance renewal cycle and more on strategizing goals for the longer term

Pursuing innovative ways to resolve claims

While readiness is vital to good outcomes, resolving claims rapidly, efficiently and compassionately is imperative to supporting individuals and businesses when losses occur.

To see this approach in action, consider what happened in New Zealand in 2023 following back-to-back catastrophic weather events. In late January and early February of last year, the Auckland, Northland and Waikato regions saw catastrophic flash flooding, with a record-breaking 161 millimeters (more than 6 inches) of rainfall within three hours. The torrential downpour was classified as a ”one-in-200-year event” by the National Institute of Water and Atmospheric Research (NIWA).

Just two weeks later, ex-tropical Cyclone Gabrielle battered the North Island, exacerbating damage — particularly along the eastern coastline — prompting New Zealand’s third-ever declaration of a national state of emergency. All told, the region received 400% of its normal February rainfall. The cyclone, estimated to be the costliest ever to hit the Southern Hemisphere, caused damages exceeding NZ$13.5 billion (about $8.2 billion U.S.) and displaced around 10,500 people.

Sedgwick subsequently received about 17,000 CAT claims covering domestic properties, commercial premises, farms and infrastructure. Leveraging longstanding relationships and global resources, we mobilized our teams, including international colleagues, and showcased the advantages of strong collaboration and scaling up swiftly. The adjusters worked tirelessly to support clients and their policyholders, utilizing innovative solutions like a custom CAT event management app and Power BI for real-time monitoring.

The response prioritized empathy and community engagement, ensuring vulnerable individuals received priority assistance. The streamlining of processes and efficient delivery of claim settlements demonstrated the power of teamwork in crisis management. Despite the massive scope of the catastrophe, more than 50% of the commercial claims were settled and closed within six months. (For more on this remarkable story, see our 2023 Major & Complex Loss Review.)

Recovery begins with resiliency

As evidenced by the experience in New Zealand, exploring options for effective recovery after climate-related catastrophes is crucial. It’s also quite challenging.

An essential component of recovering from property damage is rebuilding, and it can significantly impact the environment. According to the World Green Building Council, construction work accounts for 40% of all global emissions. Overall, the construction industry is among the world’s largest contributors to carbon emissions, with as much as 8% coming from concrete production alone. Anything we can do to lessen that carbon load as we rebuild is beneficial.

Our repair solutions teams and preferred contractor networks in the U.S. and UK are focused on identifying and promoting more environmentally-friendly options, like paint that can absorb carbon or lime plaster, which has a significantly lower carbon footprint than synthetic alternatives.

Another target area in the recovery process is repairing damage rather than doing a full replacement. It’s a sound strategy, but policyholders oftentimes expect brand-new things rather than refurbished ones. While there are issues on both sides of the repair-versus-replace debate, the first step is to think about it. Thoroughly analyze the options, conduct a cost/benefit analysis, and encourage insurers and policyholders to factor the environmental impact into their repair decisions.

Actionable data is key to informed decision-making. To help clients, our UK repair solutions division has developed an innovative carbon value calculator that identifies the environmental impact of each property claim and the related repairs by applying CO2 values to materials, labor and plant. Building on tools used to analyze the price of repairs, the carbon value calculator assigns emissions on a per-line basis, helping customers and policyholders understand the cost of each repair — not just in dollars or pounds, but in the volume of carbon produced and the impact on our planet. The one-of-a-kind calculator also simplifies and automates the traditionally time-intensive task of measuring Scope 3 emissions.

Defining Scope 1, 2 and 3 greenhouse gas emissions

According to the Greenhouse Gas (GHG) Protocol:

- Scope 1 emissions are direct emissions from sources owned or controlled by the organization. These may include on-site fossil fuel combustion and fleet fuel consumption.

- Scope 2 emissions are indirect emissions from sources owned or controlled by the organization, such as from the generation of electricity, heat or steam purchased from an energy provider.

- Scope 3 emissions are all indirect emissions not included in Scope 2 that are related to the organization’s activities and value chain.

Finding the right partner

Adapting to the impact of weather on virtually all areas of life is new to many. Awareness and education are essential, especially concerning data supporting climate change and the evolving landscape of laws, regulations, programs, policies and products. (For more, see “Climate resiliency movements: developments in ESG legislation” in Edging up.)

To help them navigate this largely uncharted territory, people and businesses are looking to partner with forward-thinking organizations that have expertise to offer and a suite of integrated services that can support their planning efforts and ensure optimal coverages are in place. Attributes to look for include:

- Climate resilience experience: Seek a partner with a demonstrated understanding of climate-related risks, the ability to tailor coverage to mitigate those risks and experience handling claims related to weather incidents.

- Green energy recognition: Ensure the organization recognizes the value of taking proactive steps, such as implementing renewable energy systems like solar panels, wind turbines and hydroelectric facilities, as well as coverage for associated infrastructure and equipment.

- Rapid claims processing: Look for businesses with a reputation for efficient claims processing, especially in the aftermath of catastrophic, climate-related incidents. Consider how they handle both the big picture and the details, such as ensuring policyholders have quick access to much-needed funds and feel supported throughout a difficult process.

- Commitment to risk assessment and mitigation: Choose a proactive partner to help prevent and minimize damage from climate-related weather incidents. Risk assessment and mitigation services may include site inspections, hazard assessments and recommendations for enhancing both property and business resilience.

- Specialized support for climate-related claims: Ensure the organization has expertise in weather-related claims challenges, assessing and valuing damage to green energy infrastructure and knowledge of relevant regulations and incentives.

Another key consideration is a demonstrated commitment to addressing climate change. Is the partner walking the walk and adopting green solutions themselves?

A good place to start is by exploring companies’ commitments to reaching carbon emission guidelines. For example, carbon net-zero status means that a country or organization aims to balance the amount of carbon emissions it releases into the atmosphere with the amount it removes through measures such as renewable energy adoption and carbon capture. The governments of the UK and U.S. have set goals to reach net-zero emissions by 2050.

In support of these commitments, Sedgwick takes the initiative to address climate change seriously. For 10 years, our UK repair solutions have held the prestigious and difficult-to-achieve ISO 14001, the international gold standard for environmental management systems. Recently, our entire UK organization earned the designation as well. In the U.S., our operations are making great strides reducing our e-waste tonnage, paper use, business travel and office footprint for the benefit of the environment. Additionally, our experts are consulting on client-focused solutions like innovative and efficient methods of reducing the ancillary, negative environmental impact of contaminated property remediation.

Extreme weather isn’t going away: ready, resolve, recover

Amid a sharp increase in climate-related disasters, the imperative for businesses to embrace readiness, resolution and recovery strategies has never been more urgent.

With environmentally focused regulations becoming more stringent, businesses and consumers may be compelled to adopt sustainable practices, rather than having the luxury to view them as optional. We all must be ready. We must find innovative ways to thoughtfully resolve climate-related losses through careful planning and an emphasis on caring for people. And, we must focus on moving beyond catastrophic weather events by finding ways to build back better: exploring green alternatives, using existing materials when possible and looking for options that will better withstand future events. It’s time to embrace recovery.

Emphasizing forward-thinking plans, processes and programs and prioritizing those measures to anticipate future needs are at the heart of climate resilience. By taking decisive steps now, businesses and individuals can lay the groundwork for a more sustainable future, while ensuring the well-being of current and future generations.

Multipronged, coordinated solutions to complex issues: a vision for the future

As with all things related to climate change, there are difficult challenges to tackle; some would tax the wisdom of Solomon, and some can even pit allies on different sides of an issue. What’s the answer for addressing complex issues? Often, it is innovation and compromise.

For example, consider a community facing the one-two punch of record-breaking heat and drought. In areas with soil with high clay content, this could lead to subsidence, or shrinkage of the subsoil and exposure of tree roots — which can damage sidewalks, underground utilities and buildings. Implementing property resilience measures can not only reduce the risk of physical damage, but also lessen the financial burden resulting from climate hazards.

At first glance, the solution is to remove the trees. Insurers know that is the best way to minimize losses and ultimately protect customers and their property. But communities often rebel against the loss of greenery. What can be done?

How about a whole new way of thinking? Insurers and businesses could, for example, work together to offset the impact of removing the trees by building a new playground, planting trees elsewhere in the community or installing an electric vehicle (EV) charging unit to promote usage. There are options; the key is to communicate, collaborate and look for alternative paths forward.