CONTRIBUTORS

JUAN CARLOS ARAIZA

Ph.D., PE, senior vice president, large and complex loss, EFI Global

CHRIS FRECHETTE

vice president, liability practice, Sedgwick

It seems like conversations around devastating weather events, rising inflation and lingering labor shortages and supply chain issues have become commonplace on the news, across boardrooms and even around dinner tables. That’s because these trends continue to affect our lives, our businesses — and even our insurance.

The trend of rising claim complexity and severity has carried into 2023, and it doesn’t appear to be slowing down anytime soon. In this article, we’ll explore some of the notable factors driving this trend and the resulting implications for the property and liability claims sectors. We’ll also share a few best practices to help insurers and other businesses better prepare for and mitigate these types of claims.

The impact of climate change and severe weather events

Around the world, we’re seeing more extreme weather conditions — resulting in an unprecedented number of claims and a higher percentage of them involving significant complexity and severity. From the record-breaking cyclone in southeastern Africa, wildfires in Chile and Canada, and unbearable heatwaves across Asia, to powerful ice storms in the southern U.S. and the latest wildfires in Maui, today’s extreme weather headlines are beginning to feel like the norm.

In fact, according to a report from insurance broker Aon, the first half of 2023 saw elevated disaster losses, with the fifth-highest economic impact on record and the highest since 2011. As of Aug. 8, the U.S. had seen 15 confirmed weather/climate disaster events in 2023 with losses exceeding $1 billion each, according to the NOAA National Centers for Environmental Information (NCEI). The report also highlights the increased frequency of these types of events; the 1980–2022 annual average was 8.1 events (adjusted for the Consumer Price Index, or CPI), and the annual average between 2018 and 2022 was 18.0 events (CPI-adjusted).

And it only appears to be ramping up, as warming temperatures and rising sea levels are projected to bring more frequent and severe natural catastrophes in the coming decades — making living situations in many places increasingly difficult and more expensive to insure.

What it all means for the insurance market

The increase in frequency and severity of weather events is reshaping the property insurance market, impacting several areas across the U.S.:

- One insurer stopped issuing new policies in California.

- Another carrier reduced property insurance coverage to homes along the east coast at risk of flooding and those in western states at risk of burning.

- Close to a dozen insurance companies in Florida went bankrupt, while other insurers have restricted coverage due to increased hurricane losses and litigation costs in the state.

- Insurance companies are declining to write policies in hurricane-prone areas of Louisiana.

Internationally, the property market remains hard, and rates continue to rise as well. According to a report from Yale Climate Connections, at least 29 billion-dollar weather disasters ravaged the world in 2022, including the European drought and heatwave, tropical cyclones such as Typhoon Nanmadol in the western Pacific, European windstorm Eunice and severe flooding like that witnessed in Pakistan and on Australia’s east coast.

The impact of complexity in construction

Another factor contributing to increasing claim complexity and severity is the human drive to push the envelope by building bigger and better. Innovation and creativity in sophisticated building design, along with new technologies and materials, continue to push the boundaries of what’s possible; they also lead to greater risk and potentially more complex claims against the manufacturers, professionals and construction companies behind the work when something goes wrong.

In an age when consumers seem to crave over-the-top luxury, novelty and destinations worthy of social media posts, design tends to stretch the bounds of aesthetic and technological precedents. Whether it’s curved steel structures, complex features like retractable roofs or specialized technologies that create truly unique experiences, the more companies deviate from standard construction procedures, the greater the level of risk they assume.

The impact of economic conditions

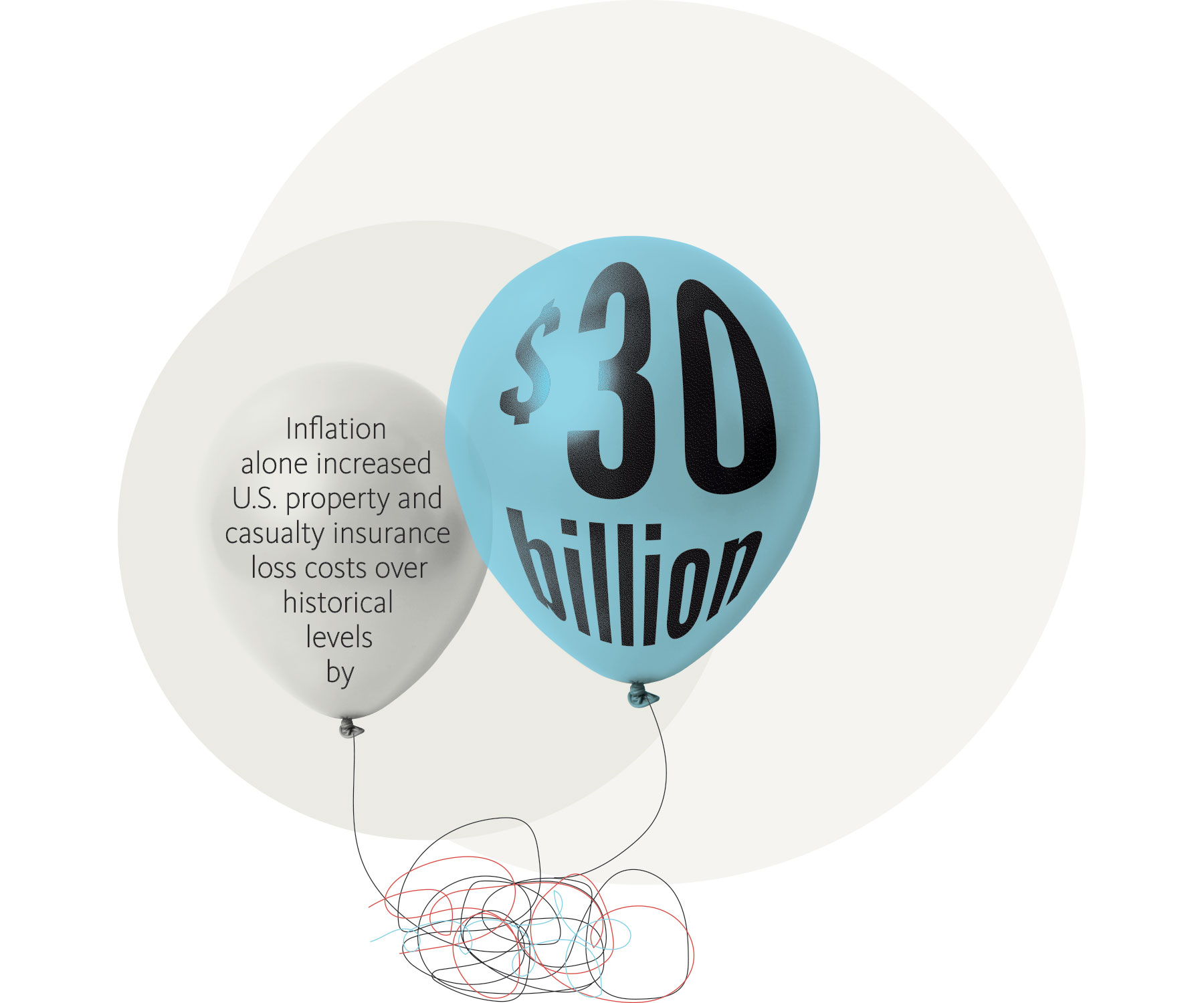

We are all too familiar with rising costs due to inflation, and the insurance industry isn’t immune to it, either. McKinsey and Company estimated that inflation alone increased U.S. property and casualty insurance loss costs over historical levels by $30 billion in 2021.

When we look at property insurance specifically, the key factors contributing to higher repair and replacement costs include labor shortages in the construction market coupled with wage inflation, extremely high demand for projects across all tiers of the industry and the rising costs of materials. Plus, the increase in uncertainty and disruption to supply chains continues to restrict the market.

The impact of litigation

We must also recognize the effects of our highly litigious society. While litigation rates across Sedgwick’s book of business remain relatively flat for new claims, an increasing number of auto and general liability claims are coming in with attorney representation earlier in the process — leaving less opportunity for resolution outside the courtroom. The impact of litigation on businesses is significant, with litigated claims accounting for as much as 50% or more of the total amount paid on all claims, depending on the line of insurance and individual mix of insured risks.

The impact of social inflation

The phenomenon of social inflation is best summed up as the explanation for how claims costs rise above pure economic inflation. In other words, the term captures the shifts in social expectations of increasingly higher claim payouts.

Why is this happening? We find juries continuing to dictate that “someone” must pay when a person is injured or a property sustains damage. And the “someone” is inevitably an entity perceived to have deep pockets. Social inflation is fueled by several factors, including:

- Third-party litigation financing, which brings outside interests into the courtroom. It can increase the duration of litigated matters and decrease the chance for plaintiff resolution in the hopes of securing an extreme verdict. Tens of billions of dollars continue to be invested into litigation funding globally, with the U.S. accounting for more than half.

- Nuclear verdicts show no sign of slowing down as juries award settlements that far surpass reasonable or expected amounts. In the U.S., these outrageous outcomes are most prevalent in product liability, auto liability and medical liability cases.

- Class action lawsuit spending has also increased for eight consecutive years and is expected to be one of the fastest-growing areas of legal spending in 2023, according to a 2023 Carlton Fields survey.

Ultimately, social inflation affects businesses through higher insurer claim payouts and loss ratios, as well as consumers through higher policyowner premiums.

Preparing for and mitigating claims: best practices

Have partnerships and plans in place

After the storm has hit is not the ideal time to start looking for loss adjusting and other disaster recovery support. Having the right partners in place before disaster strikes helps ensure policyholders, customers and other stakeholders receive priority care when it’s needed most. Make sure your partners of choice have technical expertise and are service-minded, leading with empathy during times of crisis.

It’s always best to have emergency plans and policies established in advance of a catastrophe. This helps to minimize business interruptions and expedite restoration and resolution. The most effective plans and policies include industry best practices for disasters like hurricanes and align with your insurance carrier’s specific terms and conditions. Remember to keep your plans current and put them to the test through simulations and other practice exercises. Property and facilities managers should familiarize themselves with the plans and have a clear understanding of how to properly adhere to and execute them.

Companies should also regularly review their insurance policies to ensure they’re up-to-date and reflect the current needs of the organization. We also encourage businesses to name a preferred repair solutions provider in their plans; doing so allows vendor partners to get engaged on claims as early as the first notice of loss and quickly begin remediation on water, fire and storm damage.

Employ sustainable construction practices

With devastating weather events occurring more frequently due to climate change, sustainable construction has emerged as a vital, proactive way to reduce the building industry’s adverse impact on the environment. These practices include designing for sustainability and energy efficiency and selecting materials that are locally sourced, renewable and recyclable. There is also greater focus now on water conservation through water-efficient fixtures and the inclusion of rainwater harvesting techniques. And because construction generates enormous amounts of waste, more companies are adopting waste reduction and recycling practices to decrease their environmental impact.

For organizations looking to reduce their carbon footprint, we recommend they find a partner, such as our team at EFI Global, who can evaluate their current construction practices and help them develop better strategies for optimizing sustainability.

Implement litigation avoidance strategies

Because litigation is one of the primary cost drivers in liability claims, we recommend that companies always lead with litigation avoidance. The first step is developing a risk management culture that sets the highest expectations for safe and responsible practices and processes throughout the organization.

An experienced partner can further support you with loss control consultation and assessments, deploying data and predictive analytics, and leveraging emerging technologies like telematics — all of which are useful in developing overall avoidance and mitigation plans. A cadence of regular reassessment of risks, adequacy of limits and retentions is also crucial to preparedness and understanding exposures.

We’ve also found corporate environmental, social and governance (ESG) and advocacy programs to be beneficial:

- ESG programs establish an organization’s documentable commitment to the safe and responsible conduct of its operations. The goodwill they engender helps make companies less vulnerable to being portrayed as indifferent, profit-focused institutions.

- Advocacy programs can be effective in ensuring claims examiners are communicating regularly and with empathy to claimants, always pushing toward resolution or litigating as quickly as possible.

Manage legal spend and attorney oversight

If litigation can’t be avoided, having the right partner with a strong management process for legal spending will help ensure attorneys are working on things critical for each individual case and billing according to agreed-upon standards and guidelines.

Attorney oversight is another critical best practice. Any organization going through litigation needs an effective attorney in their court. That’s why Sedgwick developed and maintains a proprietary attorney scorecard, which looks at objective measurements of different law firms and attorneys to identify high performers and support the management of overall outcomes. Scorecards offer the ability to track to litigation goals and measure the results of mitigation and management efforts. This allows clients to see where and when litigation is happening — and where we are making an impact. It also strengthens law firm relationships, which improves return on investment.

Looking forward

As we continue to face the growing challenge of managing larger and more complex claims, insurers and other businesses must keep a watchful eye on these trends and adapt their strategies accordingly. Establishing the right partnerships, having plans at the ready, and employing proactive mitigation and litigation practices are all vital to successfully navigating this evolving landscape and fulfilling our commitment to taking care of the people we serve.