CONTRIBUTORS

Max Koonce

chief claims officer, Sedgwick

David Guaragna

senior vice president, operations, Sedgwick

Price increases can be seen across all industries — from food and fuel to construction and manufacturing. When we look at the claims industry, these same factors are influencing costs in workers’ compensation, auto and property claims.

Workers’ compensation

The primary objective in the workers’ compensation process is to help injured employees recover and return to work as quickly and safely as possible. The price inflation being seen in both medical and wages may be headwinds for overall costs, yet the objective for employers must remain centered on appropriate and timely medical care with strong support for return to work.

Based on Sedgwick claims data, 2022 medical costs for U.S. workers’ compensation claims, on a per-service charge, increased an average of 3% in comparison to 2021. This was driven primarily by a 5% increase in the evaluation and management service area, a 4% increase in surgical treatment charges and a 4% increase in diagnostics charges.

In its December 2022 report, the U.S. Bureau of Labor Statistics indicated that private employer wages and benefits through September 2022 increased just over 5% compared to 2021. As of Dec. 31, 2022, the temporary total disability (TTD) daily rate for workers’ compensation claims with time away from work increased just over 5% on a national basis in comparison to 2021. Here are some additional details on increases related to TTD claims:

- Five states with the largest TTD rate increases: Vermont, Florida, West Virginia, Utah and Washington

- Three industries with the largest TTD rate increases: public sector, healthcare and retail

- Average median annual increase in the TTD weekly benefit in 2022 was 7% (Workers’ Compensation Research Institute)

Ensuring injured employees receive timely and appropriate initial and follow-up medical care, while facilitating return to work, will promote shorter durations — thereby reducing the inflationary impact of the noted headwinds.

Considerations for employers

- Maintaining a robust medical provider network for treatment of injuries will promote timely, appropriate care for injured employees.

- Cooperating with the return to work process helps drive positive outcomes.

- Providing light duty positions that fit restrictions supports the return to work process; for employers that are unable to provide modified duty positions, working with a managed care partner to find transitional work opportunities with not-for-profit organizations helps employees stay active and find purpose while they recover and reduces time away from work.

- Employers should regularly review workplace safety requirements and ensure employees are up to date on safety training focusing on injury prevention.

Auto claims

Global supply chain complications and inflation have created an environment where the standard percentages used in adjusting auto claims no longer apply. Many critical parts needed for auto repairs remain on backorder, and if the damaged cars are not safe to drive, the delay creates an extended period of time for rental cars. All of these factors, combined with price inflation, create an increase in costs.

Below are some examples of how inflation is affecting key areas in the auto industry:

- Repair costs have increased by 11% 1

- Car repairs are taking nearly twice as long to complete

- Used car values have increased approximately 40% 2

Cost containment options

A recent Sedgwick blog, Economic turmoil fuels the rising cost of auto claims, provided some suggestions to help reduce costs in auto claims. Key steps include:

- Utilize a direct repair network: A nationwide network of auto repair facilities has greater buying power than one local repair shop and may be able to secure parts faster. Leveraging a direct repair program can reduce claim durations amid part delays.

- Double down on maintenance and safety: The best way to reduce claim costs is to prevent claims from occurring in the first place. Make sure vehicles undergo proper maintenance and are in good working order — before something goes wrong and major repairs are needed. Additionally, with costs on the rise and road traffic returning to pre-pandemic levels, now is the ideal time to focus on driver safety education programs, so vehicles and their drivers can stay out of harm’s way.

Property claims

When property damage occurs, the goal is to help homeowners and businesses get repairs completed so they can resume normal living and operations as soon as possible. The repairs associated with property claims are affected by the rising costs for materials and labor, as well as supply chain issues that include manufacturing and delivery delays, labor shortages and increased fuel prices.

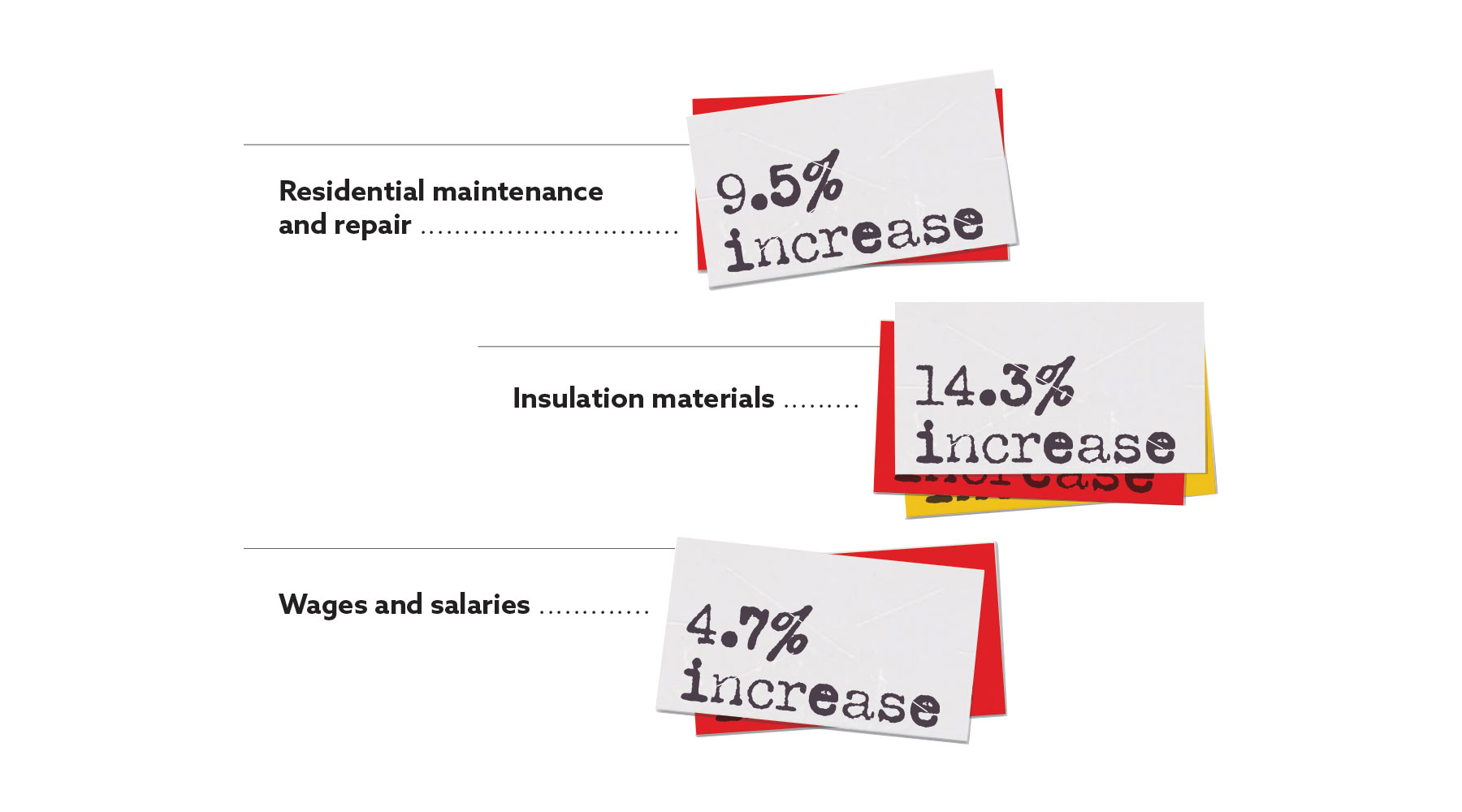

Some examples of cost increases in the construction industry, based on producer price indexes from November 2021 to November 2022, include:

Working together to mitigate costs

By ensuring all levers are being pulled and all tools are being used optimally from the start, claims teams can support clients’ cost control efforts. Ensuring prompt assignment of property claims to qualified adjusters is critical. Sedgwick’s property claims experts can verify repair costs to make sure they are correct and in line with current market pricing. Our property team helps clients with all aspects of their claims. Based on the needs of the claim, we can quickly engage additional resources, such as temporary housing specialists and building consultants. An important step homeowners and businesses can take in order to contain costs is to review their policy with their insurance representative at least twice a year to ensure the coverage is appropriate and all options have been explored.

Looking ahead

We continue to track the economic trends impacting claims and to look for every possible way to help clients mitigate claim-related costs. No matter the industry, strengthening cost-control strategies in today’s financial environment can put organizations in a better position to respond to future market trends. Watch for our upcoming state of the line reports, planned for March 2023, for more information on important issues affecting the claims sector.